On expected lines, the Reserve Bank of India (RBI) paused key policy repo rate at 5.5% on August 6, 2025, after frontloading a slew of rate cuts to the quantum of 100 basis points in the prior three policies. Accordingly, the RBI repo rate is at its lowest level in 3 years. Any change in policy rates has a direct and indirect impact on home loan interest rates, which eventually hits your pocket through EMIs on a monthly basis.

Now that the repo rate is kept steady at 5.5%, how will the new policy decision impact your home loan EMIs?

"As the RBI had front-loaded the rate category, it was expected to maintain the status quo. It is a welcome move. However, it leaves room to reconsider in the coming months as CPI is benign and a push for growth may be required. At Indian Bank, we have already passed on benefits of previous rate cut and expect further normalisation in MCLR as cost of fund continue southward journey," Binod Kumar MD & CEO of Indian Bank, told GoodReturns.

"This stability ensures that the recent 100 bps rate cut can permeate deeper in the credit markets to the advantage of both lenders and borrowers. For the housing loan market, a stable interest rate scenario ensures a risk-free choice for homebuyers and consistent growth for the housing market," said Pramod Kathuria, Founder & CEO, Easiloan.

Let's Understand The Impact Of Repo Rate On Home Loans:

What Is Repo Rate?

Repo rate is the lending rate at which the RBI lends funds to banks during a shortage of liquidity. Just like every borrower who has to pay an interest rate on their home loans, banks also have to pay an interest rate to the RBI along with the principal amount. That interest rate is the repo rate!

Repo Rate-Home Loan Link:

The repo rate has a direct impact on floating home loan rates, while it has an indirect impact on fixed home loan rates.

As per the PNB Housing website, lowering the repo rate reduces borrowing costs for the banks, encouraging them to reduce interest rates on home loans, effectively making the EMIs cheaper or reducing the loan duration.

The situation is vice versa if the repo rate is hiked!

In the case of floating rates, the majority of banks have linked their home loan interest rates with external benchmarks like the repo rate. Hence, any rise or fall in repo rate will have a direct impact on home loan floating interest rates. Meanwhile, in the case of a fixed rate, the changes in the repo rate will be felt when home loans are refinanced.

Formula For Home Loan EMIs:

P x R x (1+R)^N / [(1+R)^N-1]

P = Principal loan amount

N = Loan tenure in months

R = Monthly interest rate

The rate of interest (R) on your loan is calculated per month.

R = Annual Rate of interest/12/100

For example: If a person avails a loan of Rs 10,00,000 at an annual interest rate of 7.2% for a tenure of 120 months (10 years), then his EMI will be calculated as under:

Will Home Loan EMIs Fall After August 2025 Policy?

Home loan rates are expected to be stable after the latest policy decision.

"For borrowers, this translates directly into a period of stability, with predictable EMIs and interest rates. This also provides the banking system a crucial window to further transmit the benefits of previous rate reductions," said Amit Prakash Singh, CBO Urban Money & Co-Founder Square Yards, to GoodReturns.

But a rate cut could have boosted the already thriving housing loans market.

"A rate cut leading to a lower interest rate environment would have particularly boosted the affordable housing segment, which has been under considerable pressure in recent years," said Anuj Puri, Chairman - ANAROCK Group, after the latest status quo.

Data from ANAROCK showed that average residential prices across the top 7 cities combined have increased by 39% in the last two years alone - from INR 6,470 per sq. ft. as of Q2 2023 to INR 8,990 per sq. ft. as of Q2 2025.

Impact Of 100 Bps Cut On Bank Term Loan Rates:

Term loan interest rates, including home loans, are calculated by adding spreads to the repo rate as a benchmark. That spread is decided by banks solely.

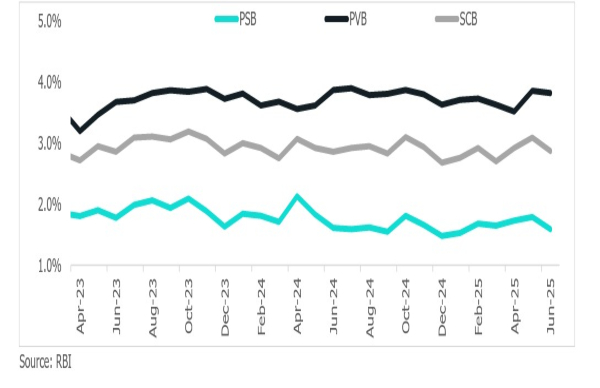

In June alone, fresh spreads declined m-o-m, with scheduled commercial banks (SCBs) falling by 22 bps to 2.87%, PVBs by four bps to 3.82%, and PSBs by 20 bps to 1.79%. The sharper drop in PSBs' spreads was driven by their more aggressive reduction in fresh lending rate following the policy rate cuts, as per the CareEdge report.

Evolution Of Spreads:

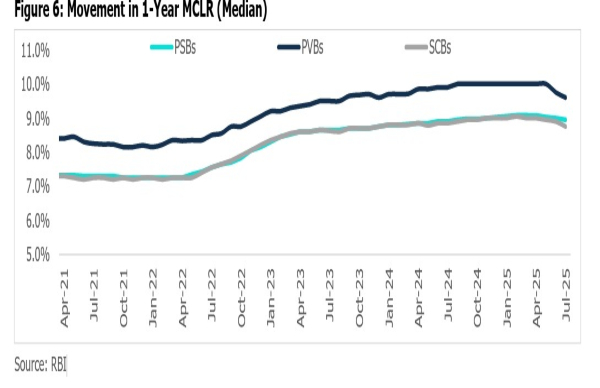

Also, the data revealed that on an m-o-m basis in July 2025, the one-year median MCLR decreased by 15 bps and stood at 8.75%, attributed to policy rate adjustments. In July 2025, CareEdge's report said, "we are seeing the effects of the lagged transmission, as deposit rates have started to decline, bringing down the MCLR across banks."

Moreover, it fell by 10 bps on a y-o-y basis and remains 55 bps above the pre-pandemic level of February 2020.

MCLR Rates Decline with rate cuts:

As of June 2025, SCBs' outstanding lending rate decreased 22 bps m-o-m to 9.45%, and PSBs and PVBs decreased by 24 and 18 bps to 8.76% and 10.47%, respectively.

The stable home loan rates are also a key positive for the real estate sector.

"A stable rate means continued affordability of home loans, especially critical in a market already seeing robust interest among mid- and premium-segment buyers," Manju Yagnik, Vice Chairperson of Nahar Group and Senior Vice President of NAREDCO- Maharashtra, said.

"For homebuyers, unchanged rates ensure continued affordability of home loans and support plans to upgrade to larger, future-ready homes," Dharmendra Raichura, VP and head of finance, Ashar Group added.

Furthermore, the latest stability in rates could boost long-term investment in real estate. Sunny Bijlani, Managing Director - Supreme Universal said, "We expect this stance to sustain demand, where buyers look for both lifestyle upgrades and long-term capital appreciation."

Notifications

Settings

Clear Notifications

No New Notifications

Notifications

Use the toggle to switch on notifications

Block for 8 hours

Block for 12 hours

Block for 24 hours

Don't block

To start receiving timely alerts, as shown below click on the Green “lock” icon next to the address bar

Click it and Unblock the Notifications

Close X

Close X

To Start receiving timely alerts please follow the below steps:

Click on the Menu icon of the browser, it opens up a list of options.

Click on the “Options ”, it opens up the settings page,

Here click on the “Privacy & Security” options listed on the left hand side of the page.

Scroll down the page to the “Permission” section .

Here click on the “Settings” tab of the Notification option.

A pop up will open with all listed sites, select the option “ALLOW“, for the respective site under the status head to allow the notification.

Once the changes is done, click on the “Save Changes” option to save the changes.

Click it and Unblock the Notifications

Click it and Unblock the Notifications